How Source of Funds Checks Work at Online Casinos

Most players understand basic verification.

A casino may ask for ID, proof of address, or confirmation that a card, bank account, or crypto wallet belongs to the person using the account. That part is familiar. It fits ordinary KYC.

Source of Funds checks are different.

They go beyond identity.

Instead of asking who the player is, the casino asks where the gambling money actually came from. That can mean salary, business income, savings, investment gains, inheritance, a property sale, or crypto profits. In other cases, it can mean tracing how money moved into the player’s bank account or how assets moved through wallets before they ever reached the casino. Regulators describe source of funds as the underlying origin of money used for a specific transaction, not just the account or wallet it arrived from.

This is where many players get caught off guard.

They assume that if the payment method is in their own name, the casino should already be satisfied. But that only proves ownership of the route. It does not fully explain the economic origin of the money. That is why licensed operators sometimes move from ordinary KYC into deeper identity and payment checks when account activity starts looking higher-risk or harder to explain. UK Gambling Commission guidance explicitly frames this as a risk-based process where the amount of information obtained and verified should rise as risk rises.

That does not automatically make the casino unfair.

But it does mean players need to understand the difference between a real compliance review and a payout-stage obstacle disguised as one.

What a Source of Funds check actually means

In simple terms, a Source of Funds check asks one question:

How did this player obtain the money being used to gamble?

That question matters because gambling operators in regulated markets are expected to prevent their platforms from being used for money laundering, criminal proceeds, and other suspicious financial activity. Regulatory guidance in both the UK and Australia describes source of funds review as part of customer due diligence and enhanced due diligence when the risk profile, transaction pattern, or account behaviour requires more scrutiny.

So the casino is not just checking whether:

- the account is yours

- the card is yours

- the bank account is yours

- the crypto wallet is yours

It may also need to check whether:

- the money is from a legitimate source

- the transaction pattern makes sense for the player profile

- the gambling activity is consistent with what the operator knows about the customer

- there are signs of third-party funding, criminal proceeds, or disguised transfers

That is the real meaning behind source of funds checks explained in a casino context. It is not only identity verification. It is financial-origin verification.

If you want to understand how operators usually build that review into the wider payout process, CasinoIndex already explains how verification often begins before a withdrawal is ever approved.

Why casinos ask where money came from

Players usually search why casinos ask where money came from only after they have already been asked for extra documents.

By that point, the check feels personal.

The casino may ask for payslips, bank statements, exchange records, tax documents, proof of a property sale, proof of business income, or evidence that supports a crypto gain. The reason is usually not random curiosity. It is tied to compliance pressure.

A regulated gambling operator sits in a high-risk payment environment. Money moves quickly, accounts can be funded from different methods, transaction patterns can change sharply, and bad actors sometimes try to make funds look cleaner by moving them through gambling platforms. Regulators therefore expect operators to collect more information when risk rises, especially in cases involving unusual, complex, or large transactions, unexplained behaviour changes, or activity with no obvious economic purpose.

That is the compliance side.

There is also a second layer.

In some jurisdictions, operators are expected to look at whether gambling activity appears consistent with what they know about the customer’s finances. The UK regulator’s player-facing guidance says gambling businesses may use bank statements, income patterns, and deposit or loss thresholds to assess legitimacy of funds and financial risk.

So when a casino asks where your money came from, the real answer is usually a mix of:

- anti-money laundering obligations

- ongoing due diligence

- transaction monitoring

- affordability or financial-risk concerns

- licensing and payment-partner pressure

That does not mean every request is fair.

It means the request has to be judged by its timing, scope, and logic.

Source of Funds is not the same as Source of Wealth

Many casinos and many players blur these two ideas together.

They are connected, but they are not the same.

Source of Funds refers to the origin of the money used for a specific transaction. Regulators describe this as how and where the funds were obtained for that transaction. Salary, business income, dividends, investment proceeds, inheritance, and sale proceeds are standard examples. They also make clear that the source of funds is not simply “the bank account” or “the wallet” the transfer came from.

Source of Wealth is broader.

It looks at how the player built their overall financial position over time. That can involve long-term employment, business ownership, investments, inheritance, property, or accumulated savings. A source of wealth review becomes more relevant when the operator doubts the wider financial background rather than just one payment event.

This distinction matters because many players think a Source of Funds request should end once they prove the bank account is theirs.

That is often not enough.

If the account activity is unusually large, inconsistent, or difficult to explain, the operator may still want evidence of the money behind the transfer, not just the transfer mechanism itself.

When Source of Funds checks usually begin

A Source of Funds check should not appear out of nowhere.

At a serious operator, it is usually triggered by a change in risk.

That can include:

A sudden increase in deposit size

If a player who normally deposits small amounts suddenly starts moving far larger sums, the account may shift into a different compliance category.

Unusual or complex transaction patterns

Regulators specifically refer to unusual patterns, unusually complex transactions, or large transactions as situations where source of funds and enhanced due diligence may become necessary.

Activity that does not match the customer profile

If the operator knows the customer as a modest recreational player and the account suddenly begins behaving like a high-value account, that mismatch may trigger review.

Withdrawal-stage review

This is where players become suspicious, and often for good reason.

Some operators are relaxed on the way in and strict on the way out. That does not automatically prove bad faith. Regulatory guidance allows ongoing due diligence and escalation when account risk changes over time. But it does mean the operator should have a clear reason for the escalation and a clear end point for the review.

Minimal gambling turnover followed by withdrawal

Regulators in Australia have even published wagering examples that specifically mention customers seeking withdrawals after minimal or no gambling turnover of deposited funds, because that kind of pattern can require closer scrutiny.

Higher-risk jurisdictions, funding patterns, or customer types

When the customer risk is higher, guidance expects stronger verification and more detailed review. That is part of risk-based and enhanced due diligence, not an optional extra.

What documents casinos may ask for

A fair review should ask for documents that actually fit the question being asked.

For salaried players, the usual request is proof of regular income. That often includes:

- recent payslips

- bank statements showing salary credits

- employment confirmation

- tax summaries

For self-employed players, freelancers, or business owners, the focus usually shifts to business-generated income. In those cases, casinos may ask for:

- business bank statements

- dividend records

- tax returns

- invoices

- accounting documents

When the money comes from savings, investments, inheritance, or another one-off event, the operator may want to see:

- savings account history

- investment statements

- proof of liquidation

- sale contracts

- solicitor letters

- inheritance documents

Operator help pages make this practical point very clearly: the documents should identify the actual source of the money used to gamble and should line up with the player’s betting or gaming activity.

That last point matters.

A good review is not just about collecting documents. It is about whether the story, the documents, and the account behaviour make sense together.

How crypto Source of Funds checks work

Crypto makes this area harder, not easier.

Many players assume crypto means fewer questions. In practice, it often means more.

The basic problem is simple: a crypto wallet can show where funds moved, but that still does not automatically explain how the player acquired those assets in the first place. If the money came from trading, staking, earlier purchases, business receipts, or transfers through several wallets, the operator may still need a credible explanation of that chain. Regulatory guidance also says more detailed verification is expected when funds come from less common sources or sources more open to criminal exploitation.

In a crypto case, a casino may therefore want to understand:

- whether the sending wallet belongs to the player

- whether the assets came from a known exchange account

- whether the transfer path is consistent

- whether the explanation matches the size of the deposit

- whether the player can support the claim with exchange history, wallet records, or transaction evidence

This is one reason crypto players should stop thinking only in terms of wallet ownership.

Wallet ownership is useful, but it is not the same as Source of Funds.

The stronger question is whether the operator can connect the deposit to a believable financial origin.

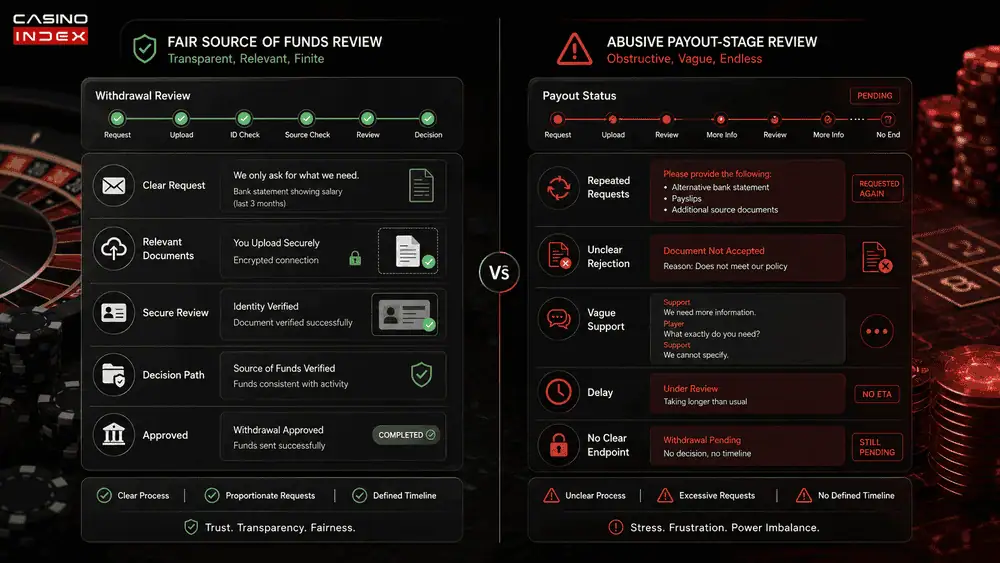

What a normal review looks like

A legitimate Source of Funds check is not pleasant, but it is usually recognizable.

It tends to be:

- proportionate to the amount and risk

- relevant to the actual concern

- limited rather than endless

- explained in a structured way

- handled by a compliance team, not vague frontline support

- connected to a real decision path

That last point is important.

A serious operator may ask for sensitive documents, but the process should move somewhere. It should not turn into a shapeless loop.

This is also where broader operator quality matters. Casinos with better controls usually communicate difficult reviews more clearly, protect documents more carefully, and create less confusion once money is under review. That is part of understanding what stronger casino-side security and account protection really look like.

What an abusive review looks like

This is where many casino articles stay too soft.

Not every Source of Funds request is fair.

Some operators appear low-friction until the player wins or requests a larger cashout. Only then does the account enter an open-ended review with shifting demands, unclear explanations, slow responses, and repeated document rejection. That pattern is not what risk-based, proportionate due diligence is supposed to look like. Regulatory guidance repeatedly stresses proportionality, targeting the customer’s actual risk, and matching the level of information to the level of concern.

The warning signs are usually practical:

- the review begins only after a meaningful withdrawal

- each document request creates another new request

- support cannot explain what is still missing

- the operator gives no clear decision path

- irrelevant material is requested

- the process stretches without visible progress

That does not prove misconduct in every case.

But the pattern matters more than the label.

A casino can call something “compliance” and still apply it badly.

Why this matters for trust and compliance at online casinos

This is where weak content usually loses the plot.

The goal is not to tell players that all checks are bad.

The goal is to explain trust and compliance at online casinos in a more honest way.

A trustworthy casino does not promise “no questions asked” forever. That promise may sound attractive, but in real money environments it can also signal weak controls, weak licensing pressure, or weak payout discipline.

A stronger operator is usually more honest.

It tells players that deeper checks may happen when activity changes, when transactions become unusually large, or when the source of funds is unclear. It does not need to ask for everything at once. But when it escalates, the logic should still be visible.

That is also why licensing matters so much. If you want to judge whether an operator is likely to run serious checks in a proportionate way or improvise them badly under pressure, it helps to understand how licensing standards shape real player protection and financial review practices.

Final thought

Source of Funds checks are not automatically a red flag.

In regulated gambling, they exist because operators are expected to understand who their customers are, how the money is being used, and whether transactions make sense in context. Authorities in the UK and Australia both frame this as part of risk-based customer due diligence and enhanced monitoring, especially where behaviour becomes unusual, large, or hard to explain. Enforcement actions have also shown that regulators do punish gambling operators for weak identity and fund-source controls.

The real issue is not whether a casino has Source of Funds checks.

The real issue is what those checks look like when the money matters.

If the process is proportionate, relevant, documented, and finite, it can be part of a serious compliance system.

If it appears only when you try to cash out, keeps changing shape, and never seems to move toward resolution, that is where players should stop seeing it as routine verification and start treating it as a trust signal in itself.